The present value of an annuity is the amount of money needed today to cover future annuity payments. Money received now is worth more due to the time value of money. The present value calculation considers the annuity’s discount rate, affecting its current worth.

Need Help Accessing Your Money?

Start with a no-obligation estimate and a guarantee that we will beat any valid offer.

Terry Turner Senior Financial Writer and Financial Wellness Facilitator Terry Turner is a senior financial writer for Annuity.org. He holds a financial wellness facilitator certificate from the Foundation for Financial Wellness and the National Wellness Institute, and he is an active member of the Association for Financial Counseling & Planning Education (AFCPE®). Read More

Savannah Pittle Senior Financial Editor Savannah Pittle is an accomplished writer, editor and content marketer. She joined Annuity.org as a financial editor in 2021 and uses her passion for educating readers on complex topics to guide visitors toward the path of financial literacy. Read More

Timothy Li, MBA Business Finance Manager Timothy Li, MBA, has dedicated his career to increasing profitability for his clients, including Fortune 500 companies. Timothy currently serves as a business finance manager where he researches ways to increase profitability within the supply chain, logistics and sales departments. Read More

Fact Checked Fact CheckedAnnuity.org partners with outside experts to ensure we are providing accurate financial content.

These reviewers are industry leaders and professional writers who regularly contribute to reputable publications such as the Wall Street Journal and The New York Times.

Our expert reviewers review our articles and recommend changes to ensure we are upholding our high standards for accuracy and professionalism.

Our expert reviewers hold advanced degrees and certifications and have years of experience with personal finances, retirement planning and investments.

How to Cite Annuity.org's ArticleAPA Annuity.org (2024, July 30). Present Value of an Annuity: Formulas, Calculations & Examples. Retrieved September 9, 2024, from https://www.annuity.org/selling-payments/present-value/

MLA "Present Value of an Annuity: Formulas, Calculations & Examples." Annuity.org, 30 Jul 2024, https://www.annuity.org/selling-payments/present-value/.

Chicago Annuity.org. "Present Value of an Annuity: Formulas, Calculations & Examples." Last modified July 30, 2024. https://www.annuity.org/selling-payments/present-value/.

Why Trust Annuity.org Why You Can Trust Annuity.orgAnnuity.org has been providing reliable, accurate financial information to consumers since 2013. We adhere to ethical journalism practices, including presenting honest, unbiased information that follows Associated Press style guidelines and reporting facts from reliable, attributed sources. Our objective is to deliver the most comprehensive explanation of annuities, structured settlements and financial literacy topics using plain, straightforward language.

We partner with CBC Settlement Funding, a market leader with over 15 years of experience in the settlement purchasing space. Our relationship with CBC allows us to facilitate the purchase of annuities and structured settlements from consumers who are looking to get a lump sum of cash immediately for their stream of monthly payments. When we produce legitimate inquiries, we get compensated, in turn, making Annuity.org stronger for our audience. Readers are in no way obligated to use our partners’ services to access Annuity.org resources for free.

CBC and Annuity.org share a common goal of educating consumers and helping them make the best possible decision with their money. CBC is a Better Business Bureau-accredited company with an A+ rating and a member of the National Association of Settlement Purchasers (NASP), a national trade association that promotes fair, competitive and transparent standards across the secondary market. Additionally, Annuity.org operates independently of its partners and has complete editorial control over the information we publish.

Our vision is to provide users with the highest quality information possible about their financial options and empower them to make informed decisions based on their unique needs.

Understanding the present value of an annuity allows you to compare options for keeping or selling your annuity.

It lets you compare the amount you would receive from an annuity’s series of payments over time to the value of what you would receive for a lump sum payment for the annuity right now.

Annuity Payments Over Time vs. One Lump Sum Payment Now

“The present value of an annuity is affected by factors such as the interest rate used to discount future payments, the number and amount of payments and the timing of the payments,” Rhett Stubbendeck, CEO of LeverageRX, told Annuity.org.

It’s critical that you know these amounts before making financial decisions about an annuity. There are formulas and calculations you can use to determine which option is better for you.

Factoring companies, or companies that will buy your annuity or structured settlement, use discount rates to account for market risks such as inflation and to make a small profit for granting you early access to your payments. A discount rate directly affects the value of an annuity and how much money you receive from a purchasing company.

Standard discount rates range between 9% and 18%. They can be higher, but they usually fall somewhere in the middle. The lower the discount rate, the higher the present value. Low discount rates allow you to keep more of your money.

According to the Internal Revenue Service, most states require factoring companies to disclose discount rates and present value during the transaction process. Always ask for these numbers before you agree to sell payments.

DID YOU KNOW?State and federal Structured Settlement Protection Acts require factoring companies to disclose important information to customers, including the discount rate, during the selling process.

It’s also important to note that the value of distant payments is less to purchasing companies due to economic factors. The sooner a payment is owed to you, the more money you’ll get for that payment. For example, payments scheduled to arrive in the next five years are worth more than payments scheduled 25 years in the future. Keep this in mind during the selling process.

Need to Sell Your Annuity for Cash Immediately?

Stop waiting for future payments. Sell your annuity or structured settlement for a lump sum now. Get a no-obligation quote today and explore your options.

The present value of an annuity is based on a concept called the time value of money — the idea that a certain amount of money is worth more today than it will be tomorrow. This difference is solely due to timing and not because of the uncertainty related to time.

Simply put, the time value of money is the difference between the worth of money today and its promise of value in the future, according to the Harvard Business School.

Payments scheduled decades in the future are worth less today because of uncertain economic conditions. In contrast, current payments have more value because they can be invested in the meantime.

That’s why $10,000 in your hand today is worth more than $10,000 over the next 10 years.

If you own an annuity or receive money from a structured settlement, you may choose to sell future payments to a purchasing company for immediate cash. Getting early access to these funds can help you eliminate debt, make car repairs, or put a down payment on a home.

Companies that purchase annuities use the present value formula — along with other variables — to calculate the worth of future payments in today’s dollars.

Calculating present value is part of determining how much your annuity is worth — and whether you are getting a fair deal when you sell your payments.

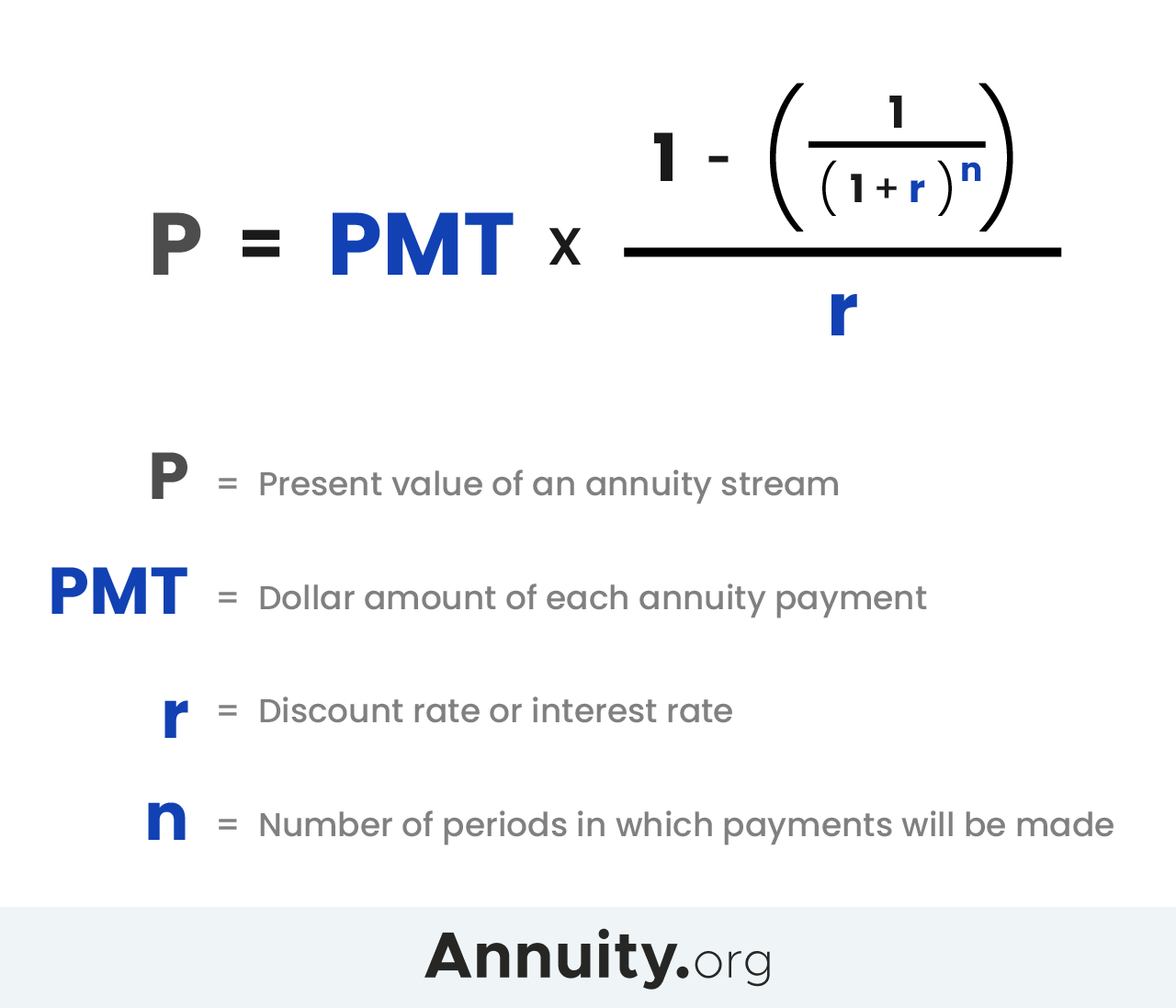

In order to understand and use this formula, you will need specific information, including the discount rate offered to you by a purchasing company.

The information you need when using the present value formula:

You can plug this information into a formula to calculate an annuity’s present value.

Present value calculations are influenced by when annuity payments are disbursed — either at the beginning or at the end of a period. These are called “ordinary annuities” if they are disbursed at the end of a period, versus an “annuity due” if payments are made at the beginning of a period.

An ordinary annuity is typical for retirement accounts, from which you receive a fixed or variable payment at the end of each month or quarter from an insurance company based on the value of your annuity contract.

To calculate the present value of an annuity due, use this formula:

Annuity due refers to payments that occur regularly at the beginning of each period. Rent is a classic example of an annuity due because it’s paid at the beginning of each month.

To calculate the present value of an annuity due, use this formula:

Interested in Selling Annuity or Structured Settlement Payments?

Turn your future payments into cash you can use right now.Many websites, including Annuity.org, offer online calculators to help you find the present value of your annuity or structured settlement payments. These calculators use a time value of money formula to measure the current worth of a stream of equal payments at the end of future periods.

Simply enter data found in your annuity contract to get started. In just a few minutes, you’ll have a quote that reflects the impact of time, interest rates and market value.

What you’ll need to use our calculator:

This estimate is a great first step. It gives you an idea of how much you may receive for selling future periodic payments.

However, it isn’t perfect.

Learning the true market value of your annuity begins with recognizing that secondary market buyers use a combination of variables unique to each customer.

That’s why an estimate from an online calculator will likely differ somewhat from the result of the present value formula discussed earlier.

Secondary market buyers consider other variables, including:

Use your estimate as a starting point for a conversation with a financial professional. Discuss your quote with one of our trusted partners, who can explain the present value of your payments in more detail.

It’s also important to keep in mind that our online calculator cannot give an accurate quote if your annuity includes increasing payments or a market value adjustment based on fluctuating interest rates.

Email or call our representatives to find the worth of these more complex annuity payment types.

Let’s Talk About Your Financial Goals.

Take our free 3-minute quiz to match with a financial advisor instantly. Recommendations tailored to your goals.

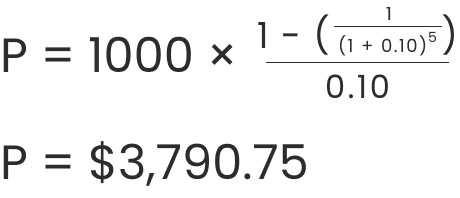

Let’s say your structured settlement pays you $1,000 a year for 10 years.

If you keep all your payments, you will eventually receive $10,000.

But what if you lose your job and need more than $1,000 a year to cover your expenses?

Let’s assume you want to sell five years’ worth of payments, or $5,000, and the factoring company applies a 10 percent discount rate.

In this example,

Therefore, the present value of five $1,000 structured settlement payments is worth roughly $3,790.75 when a 10% discount rate is applied.

If you simply subtract 10% from $5,000, you would expect to receive $4,500. However, this does not account for the time value of money, which says payments are worth less and less the further into the future they exist. That’s why the present value of an annuity formula is a useful tool.

There are several factors that can affect the present value of an annuity. Most of these are related to the annuity contract dealing with interest rates, guaranteed payments and time to maturity. But external factors — most notably inflation — may also affect the present value of an annuity.

Interest Rates An annuity’s interest rate is used to discount future payments. The discount rate reduces future cash flow from the annuity. So, the higher the interest rate is, the lower the annuity’s present value will be.

Payment Amount and Frequency Since the present value of an annuity is the value of future payments, the more payments you have and the higher each payment is, the greater your present value will be.

Time to Maturity This is the time until payments are received from the annuity. The longer the wait until payments are received, the more time it has for compound interest to build value in the annuity. This longer time period will increase the annuity’s present value.

Inflation Inflation or other external factors can erode the future value of an annuity. When you take inflation into account, it can reduce the present value of an annuity.

It’s critical to know the present value of an annuity when deciding if you should sell your annuity for a lump sum of cash.

“Knowing the present value of an annuity is important because it allows you to understand the value of future payments in today’s dollars,” Stubbendeck said. “This knowledge can help with financial planning, investment decisions and assessing the overall value of the annuity.”

4 Reasons You Need To Know the Present Value of an Annuity

Understanding the Value of Future Payments The present value of an annuity represents the value of the future payments you will receive in today’s dollars. By calculating the present value of your annuity, you can determine how much your future payments are worth in today’s money and make informed financial decisions.

Evaluating Offers To Sell Your Annuity If you are considering selling your annuity, understanding its present value can help you evaluate offers from buyers and determine whether they are fair and reasonable.

Making Retirement and Financial Planning Decisions The present value of an annuity is a key factor in retirement and financial planning. By knowing the present value of your annuity, you can plan your retirement income and make informed decisions about your future finances.

Understanding Tax Implications Knowing the present value of your annuity can also help you understand the tax implications of selling or holding onto your annuity. Depending on the situation, selling an annuity can result in a tax liability, and understanding the present value can help you determine the tax consequences of selling.

Join Thousands of Other Personal Finance Enthusiasts

Get personal finance tips, expert advice and trending money topics in our free newsletter.Annuity calculators, including Annuity.org’s immediate annuity calculator, are typically designed to give you an idea of how much you may receive for selling your annuity payments — but they are not exact.

The actual value of an annuity depends on several factors unique to the individual who’s selling the annuity and on the variables used for the buying company’s calculations.

What is the present and future value of an annuity?The present value of an annuity represents the current worth of all future payments from the annuity, taking into account the annuity’s rate of return or discount rate. To clarify, the present value of an annuity is the amount you’d have to put into an annuity now to get a specific amount of money in the future.

The future value of an annuity is the total amount of money that will build up over time, including all payments into the annuity and compounded interest over its lifetime.

Together, these values can help you determine how much you need to put into an annuity to generate the types of income streams you want out of it.

What is an example scenario for calculating the present value of an annuity?As an example, let’s say your structured settlement pays you $1,000 a year for 10 years. You want to sell five years’ worth of payments ($5,000) and the secondary market buying company applies a 10% discount rate.

Using the formula on this page, the present value (PV) of your annuity would be $3,790.75.

This can give you a starting point when considering whether to sell your annuity.

Annuity Table A tool for calculating the present value of an annuity. For this reason, it is also sometimes called a present value table.

Learn More: Annuity Table for an Ordinary AnnuityAnnuity Issuer The insurance company that sells the annuity and pays the income benefits. The issuer assumes the financial risk in exchange for annuity premiums.

Learn More: Best Annuity Companies of 2024Structured Settlement Protection Act (SSPA) Passed in 1997, these state-defined laws originated in Illinois and regulate the secondary market.

Learn More: Structured Settlement Protection Acts Please seek the advice of a qualified professional before making financial decisions. Last Modified: July 30, 2024